If you’ve ever looked at your savings and wondered whether it’s really enough, you’re in good company. Between rising living costs, changes at work, and the occasional emergency repair, it can be hard to know what the right number should be.

There isn’t one perfect savings amount that fits every household in Central Illinois. A family in Effingham has different expenses than someone in Edwardsville or Newton, and every household has its own rhythms. That’s why financial experts often recommend using a simple framework to help Illinois families set a realistic emergency savings goal for 2026.

Below, we break down what that framework looks like, how to calculate your own number, and explore the question “How much should I save in Illinois?” based on different family situations and goals.

Why Savings Feel Extra Important Going Into 2026

The last few years have brought a rollercoaster of rising prices, disruptions in childcare, shifting jobs, and unexpected expenses. While these aren’t new challenges, many families are feeling them more sharply than before. That makes 2026 the right moment to revisit your emergency savings plan.

A strong emergency fund isn’t about expecting the worst, it’s about giving yourself breathing room when life throws a curveball. Think of it as your financial safety net. You might not need it every day, but it’s a lifesaver when the unexpected happens.

What Experts Usually Recommend Saving

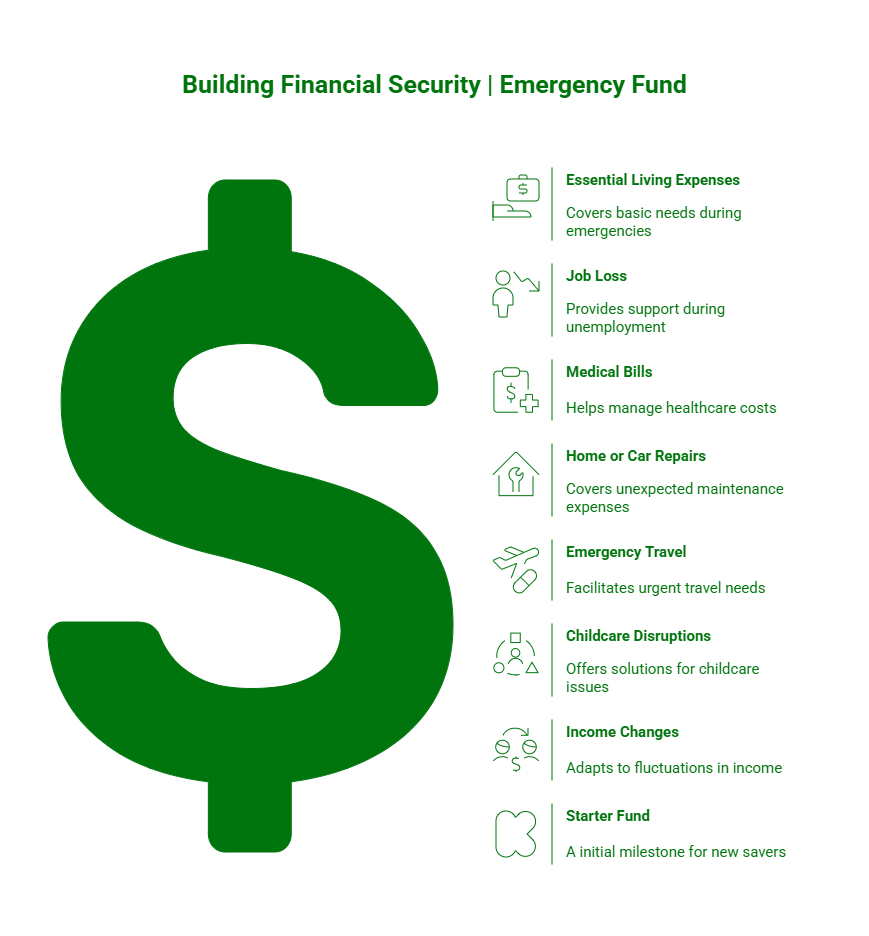

Most financial advisors agree that families should keep three to six months of essential living expenses in an emergency fund, which helps you stay afloat during job loss, medical bills, home or car repairs, emergency travel, temporary disruptions in childcare, and sudden changes in income.

For many households, building an emergency fund Illinois families can rely on is an important step toward financial stability.

Families with children, single-income households, and people with variable or seasonal income (common across rural Illinois communities) are often better off aiming toward the higher end of that range or even saving up to a full year of expenses.

What about if you’re just starting out? A starter emergency fund of $1,000–$2,000 is a great first milestone. This can cover those frustrating but common emergencies like a new tire, a surprise veterinary bill, or an insurance copay.

How to Calculate Illinois Family Savings 2026 Goals

Every Illinois household has a different “right number,” but here’s the simplest way to find yours.

1. Add up your essential monthly expenses.

Include only what it takes to run your household. Consider the following list as you add:

- Housing

- Groceries

- Utilities

- Gas and transportation

- Childcare

- Medical costs

- Insurance

- Debt payments

- Household basics

- Internet and phone

This number represents the baseline cost of your life each month.

2. Multiply that number by 3–6.

This gives you a recommended emergency savings range. For example, if your essential expenses are $3,000 a month, your emergency fund goal would be $9,000–$18,000. If your expenses are closer to $5,000 a month, your range moves to $15,000–$30,000.

3. Adjust up if you have added risks.

If you answer “yes” to any of these, it may be wise to build toward 6–12 months of savings:

- You rely on seasonal or unpredictable income

- Your household has one primary income

- You have young children or high childcare costs

- You’re self-employed or work in the gig economy

- You live in or near a higher-cost area

4. Add long-term savings after your emergency fund.

Your emergency fund is your foundation, and once it is in place, you can start saving for longer-term goals such as education, retirement, travel, or future purchases. Many families find it helpful to use different savings accounts for different goals, so everything stays clear and easy to manage.

Why This Savings Framework Makes Sense in 2026

Between economic uncertainty, shifting employment trends, and rising household costs, it’s no surprise that Illinois families are aiming to save more than before. A healthy emergency fund provides stability, allowing you to handle layoffs, schedule changes, or medical surprises without panic. It also offers freedom from debt, reducing the need to rely on high-interest credit cards during emergencies, and peace of mind, making even the unexpected feel more manageable.

Beyond covering immediate needs, having a solid savings buffer gives you room to grow financially, so once essentials are taken care of, you can confidently pursue bigger goals. Developing a clear budget can make that process feel more manageable and help you stay consistent along the way.

Realistic Savings Targets for Central Illinois Households

Different households need different savings amounts, and understanding your unique situation is key to estimating your ideal emergency fund. If you have a stable income and no dependents, one to three months of expenses may be sufficient, while a two-income family with children typically benefits from three to six months of savings.

Households relying on a single income or with unpredictable work circumstances may want to aim for six to nine months, and self-employed individuals or those in the gig economy might need nine to twelve months to stay financially steady during slow periods.

For many Illinois households, from Dieterich to Effingham to Red Bud, this often translates to roughly $15,000 to $35,000 in liquid savings, depending on monthly expenses and risk factors. Ultimately, your ideal number might be higher or lower, but what matters most is that it reflects your family’s specific needs and lifestyle.

How to Build Your Savings, Even If You’re Starting Small

Saving several months of expenses can sound overwhelming, but it’s built one step at a time. Even starting today with a small amount can make a meaningful difference over time.

Here are realistic ways families can get started:

- Set up small automatic transfers, even $25 or $50 at a time.

- Keep your emergency savings in a separate account so you’re not tempted to dip into it.

- Build a small buffer first ($1,000–$2,000) before aiming for the full amount.

- Add more during higher-income months if your work is seasonal.

- Use tax refunds, bonuses, or unexpected income to give your fund a boost.

- Keep your emergency fund liquid and easy to access and not tied up in long-term investments.

Tip: Take advantage of Dietrich Bank’s Green Cents savings account, where transactions are automatically rounded to the nearest dollar and deposited into savings!

Why Illinois Families Trust Dieterich Bank

For generations, we’ve worked alongside families in our communities, helping them plan for both expected milestones and unexpected moments. From day-to-day saving to preparing for life’s changes, our goal is to help people feel confident about their financial decisions.

Whether you live in Effingham, Teutopolis, Newton, Red Bud, Edwardsville, St. Elmo, or a nearby rural community, our focus is the same. We offer straightforward tools, local guidance, and support designed to fit real life, not a one-size-fits-all approach.

We care about growing with our communities by helping families save consistently, prepare for the unexpected, and work toward the goals that matter most to them.

Take the Next Step Toward a Strong 2026

If you’re ready to start building your emergency savings, we’re here to help. Finding the right savings account or CD can make it easier to stay consistent and keep your goals on track.

Have questions or want guidance?

You can reach out to your local branch or explore your options online whenever it’s convenient. Taking small steps now can make a real difference when life throws a surprise your way.